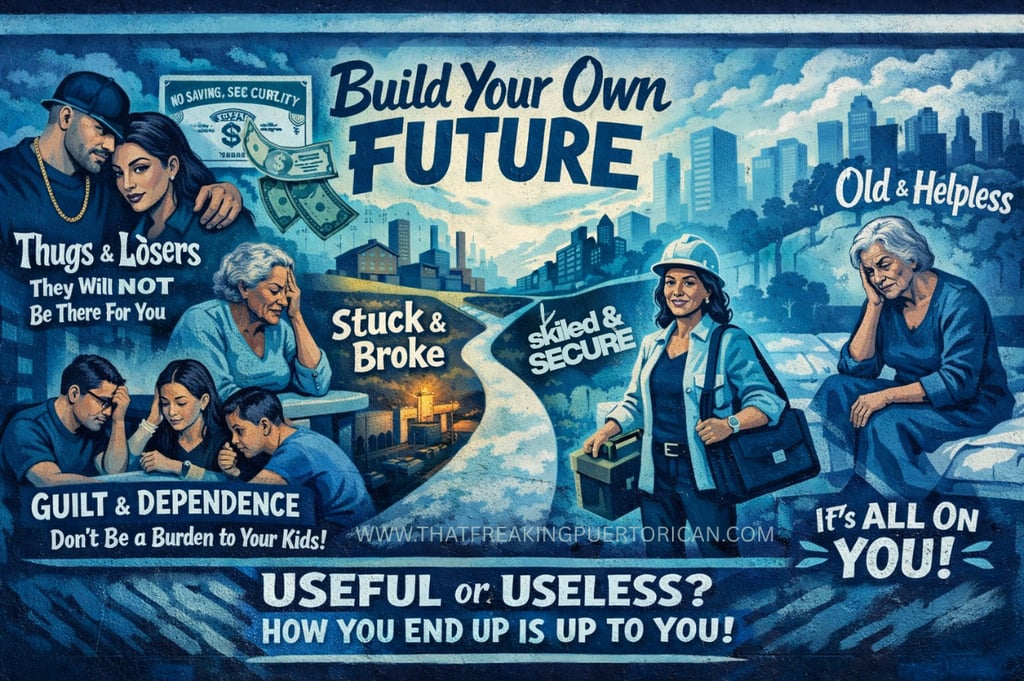

Build our Own Future

A look into your life in the long run. What to expect with your SSI and what you can do to further enrich your golden years.

Most people aren’t paying attention, but they should be. The longer we stay trapped in low-paying jobs, unstable work, or hustle culture, the more our Social Security nest egg quietly simmers on the back burner. And for a huge chunk of Americans, that pot is damn near empty.

Why? Because most of us are stretched way too thin. Rent or mortgages eat first. Utilities, groceries, transportation, kids, and emergencies eat second. What’s left? Almost nothing. So people start cutting corners. Off-the-books work. Odd jobs. Cash hustles. Side moves that help today but never get reported, never get taxed, and never count toward Social Security.

It feels like survival in the moment. But long-term? That decision comes back with teeth and it will bite you in the ass.

To even qualify for Social Security retirement benefits, you generally need to work at least 10 years, which equals 40 work credits, and you must pay Social Security taxes on those earnings. Sooo, if you've earned more than $7,500 annually for the majority of your adult life, then you already qualify. The goal here is to aim at higher income opportunities for a better tomorrow.

Now, granted, higher numbers work in our favor when it ones time for calculations. But the summary above is just the entry ticket. The actual payment you receive is a whole different story. This, my fellow Boricuas, isn't taught, this entire work ethic is a solid trait that is instilled into the minds of your offspring as they grow. It becomes woven into their train of thought... take heed:

Social Security doesn’t calculate your benefit based on your best decade. It’s based on your highest 35 years of earnings. If you worked fewer than 35 years, the missing years are counted as zeroes. Zero income years drag your average down hard, which means a lower monthly check for the rest of your life.

Here’s how the credit system works. You earn credits by working and paying into Social Security. In 2026, you earn one credit for every $1,890 in reported earnings, up to a maximum of four credits per year. You need 40 credits total to qualify, and they do not have to be consecutive. Take breaks if you need to, but understand the math never forgets.

There are exceptions. Disability benefits may require fewer credits for younger workers. But for standard retirement? The rule is simple. The more years you work, up to 35, and the higher your earnings during those years, the higher your monthly benefit will be. Period.

You can and should check your own Social Security record. Go directly to the Social Security Administration’s website, create a free account, verify your email, and review your estimated benefits. No guessing. No assumptions. Just your real numbers, staring back at you.

This part needs to be said plainly, especially to Hispanic women who were taught—explicitly or quietly—to rely on a man or to cash in youth and beauty instead of building stability.

Do not bet your future on a man. Do not waste your prime years orbiting chumps, dead weight, or lowlife thugs thinking loyalty or looks will age into security. They will not be there for you. Love doesn’t pay rent at 65. Charm doesn’t cover prescriptions. And nostalgia won’t replace a missing income stream.

And here’s the other side no one likes to talk about.

If you are a mother who failed to plan, failed to build, and now survives by guilt-tripping your adult children—wedging yourself into their lives through manipulation, obligation, or emotional leverage—that is not wisdom. That is dependence disguised as authority.

At that point, you didn’t “age into respect.” You aged into liability.

When a parent clings to their grown children because they squandered their youth, avoided accountability, and never secured skills or savings, the role reverses. You go from parent to dependent. And no, it is not automatically your child’s responsibility to subsidize bad decisions made decades earlier.

The most honorable move as you age is this: make yourself useful. Contribute. Add value. Bring skill, support, money, or stability into the lives around you—not stress, not need, not entitlement.

An older person with no skills and no money must at the very least ensure they are not draining the prosperity of others. It is not “heartless” to say this. It is reality.

Sound harsh? It is. But how you end up is not random. It is the cumulative result of choices made over a lifetime. Plan accordingly.

This is where the uncomfortable truth hits.

A good job, a real career, or a solid trade is light-years better than the average meat-puppet / brain-dead end job. Not because of ego. Because of math. Because one day your body won’t cooperate the way it does now.

You do NOT want to be old, achy, and broke. BUZZER—Full stop. Nobody wants to be choosing between medication, food, or heat at 70 years old. That’s failure by neglect. THE ELDERLY IN DEPLORABLE CONDITIONS is oftentimes an avoidable scenario. And while certain living situations are beyond our control, other upcoming cases are brewing that are well within our means of "repair", so to speak. So, it's NEVER TOO LATE TO FIX THINGS FOR THE BETTER.

Improve your income today. Make gains now. Learn a trade. Level up your skills, even if you are up there in years. Take the job that pays more even if it’s uncomfortable at first. Do it for yourself, love, because Social Security is literally your security as you age within society. Add to it or regret it later on.

Ignore this long enough and you don’t just fall behind. You fall straight through the cracks.